Welcome to Part 2/2 of our Negotiation In Sales Clinic.

If you missed part 1, here’s a brief recap of what we covered How To Win The Negotiation Before It Starts:

- Know your leverage with the 3 why's: Why buy at all, buy you, and buy now?

- Give price then shut up: Explain how pricing works, give price, stop talking.

- Win vendor of choice independent of price: Why negotiate to lose anyway?

Now that you’re vendor of choice, you need to finish the negotiation in one cut. Here’s how we’re breaking it down in another 3 steps to finish the series:

- Lock down your deal

- Get the full and final ask

- Use options and tradeoffs to close in 1 cut

Let’s land this plane.

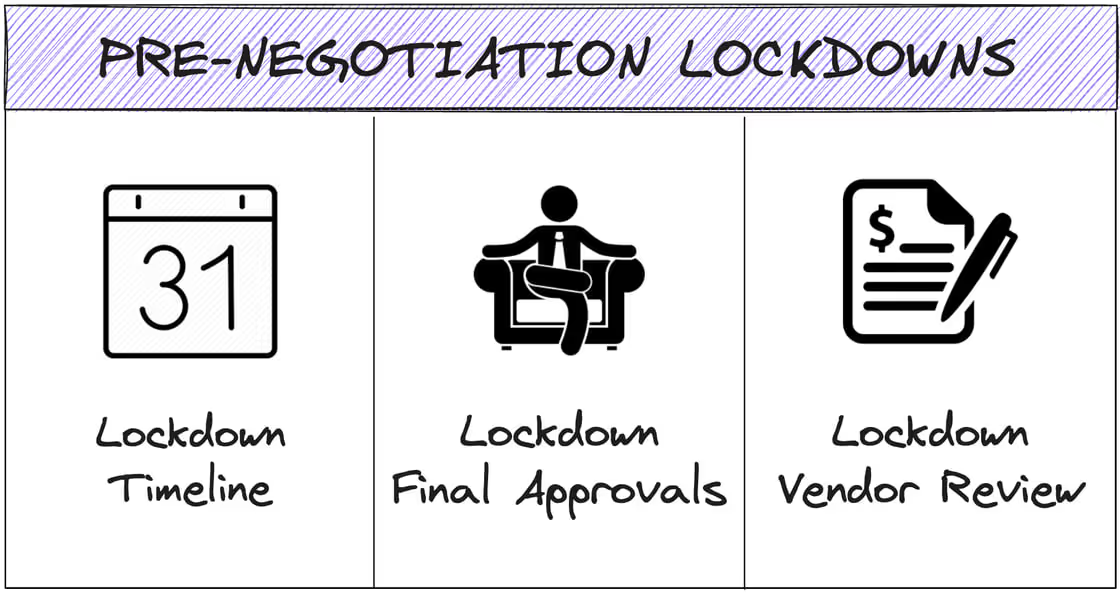

Step 1: Lock down your deal

Ever give a discount, then the deal slips anyway? That happens when reps:

- Extend a discount without getting explicit agreement on timeline

- Agree on a timeline that can’t actually be met

Use a basic give-get for commitment on timeline. Whenever you give something up you should always get something in return. Create a cost to every ask in a negotiation so that you don’t die from death by a million cuts.

I'll often say: "But before I bring anything back to my CFO, the first question I’m going to get asked in return is if this gets it done within the period. Let’s pretend we can come to an agreement, are you in a position to sign by [DATE]?"

But then get explicit agreement on everything else that needs to happen first (ie: executive approvals, legal review, security review). Walk through every step and get agreement on the steps that happen after we agree on commercials.

You have to share the consequences of a slip upfront. If they “try their best” and you take away the discount when the deal slips, it comes off as super shady if you didn't discuss that upfront.

I'll usually say: "Jane, I hate to bring this up, but I don’t want you to have a bad taste in your mouth in the worst case scenario. If I get approval from my CFO and this crosses into next month, he’s going to want to revisit the deal."

Make it clear, trying their best does not seal the deal.

Step 2: Get the full and final ask

In the middle of the ‘22 tech crash, a brutal CFO fought me to death. She had 5 competitive quotes, anchored me at a 50% discount, and barely moved an inch.

After a long, long negotiation, I eked out a commitment on a 20% discount. (whew, safe)

Then she immediately said… “Great. Now I want monthly payments.”

(You’re kidding me. I gotta go through that entire thing again… for billing terms now!?)

A savvy buyer knows to take the biggest bite out of the price… then ask for everything else. So always get the full ask before negotiating the deal:

- Ask what number gets it done (if they don’t, try this). “My CFO's going to ask if this actually gets it done. If I don't have a number, he’s gonna look at me and say “Armand, I can’t do anything for you here.”

- Delay the negotiation and ask what else? “We give all of our proposals in one cut. If we go rock bottom on price, we won’t have any flexibility on things like billing terms or anything else. So what else stood out for you in the proposal?”

Then make it really painful to get the final ask. If you give too easy, they'll keep asking for more. My 3 tactics to make the negotiation feel like work are that (in no particular order):

- Start with price and “fake the walk” for lowballs: “I just know we’re too far off. I guess on that basis it’s not even worth me going back to my team then, right?”

- Remove value in exchange for price: My realtor did this exceptionally well: “If I drop my commission, are you okay with me doing 2 fewer open houses and spending less on the professional photos?”

- Ask for something every time they ask for something: Never give unilateral concessions. If they ask for rate locks, you ask for a multi-year deal. If they ask for volume discounts, you ask for more seats.

Stay in the fight for a solid 5-10 minutes. They’ll start to show flexibility on their asks and raise their number. Once they do, that’s when you seal the deal.

Step 3: Use Options and Tradeoffs to Finish The Deal

Eventually, you need to stop asking them questions and pushing back and drive toward a solution. Here are the steps I take to do that.

First, confirm the number. If they gave you a fair number, allude to the fact that you think you can get that approved. If they’re still too low, I like to “soft float” a number to get them to bite. For example, if they’re at $35k, I’ll say “I think I can get a 4 in front of it.”

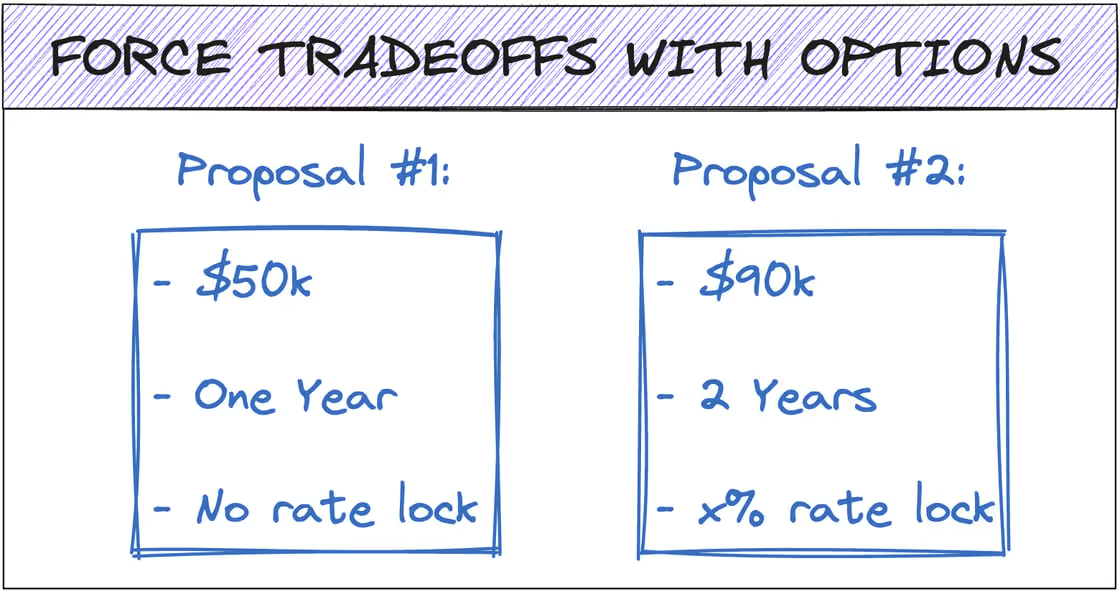

Use options give them perceived control: Don't ask a kid to put on their shoes, ask if they want their red shoes or blue shoes. People feel in control with options. Come up with 2-3 options to propose to finance that include all terms discussed.

Within the options, create tradeoffs with popcorn pricing (creds to Belal Batrawy). Create a board where no matter what option they pick, you win. For example, if they care about price and a rate lock, but you care about the total contract value and get paid more for multi-year deals, you could steer them in either direction:

- You could offer a $50k one-year deal with no rate lock (you get the biggest single year deal and they avoid the multi-year commitment)

- You could offer a $90k multi-year deal with a rate lock (they get the rate lock and a discount but you get paid more for the multi year deal)

Get commitment on an option, then go to your “team” for approval (even if you approve the deals). Play up the process and make it clear that their commitment is what gets your CFO’s approval. I even did this as a VP of Sales.

That’s how you get it done in one cut.

***

It’s not easy selling nowadays folks. Pre-2022 I sold no-discount deals all the time. Post-2022 I found myself happy getting away with 20% at times.

But regardless of the economic climate, the principles of making a negotiation feel like work and using options to drive to close quickly hold true.

If you liked this, we just dropped the second episode in our 2 part special with FBI negotiator Chris Voss – and it’s all about getting to the final agreement: